Individual income tax in China is the tax paid on personal income, being distinct from the tax paid on the company’s earnings. Normally, the remuneration obtained by a foreign employee while working in China (paid by domestic/foreign companies or other employers) is considered income derived from China. IIT (individual income tax) is paid depending on how much the expat in China earns, who bears his/her income, how long he stays here and the positions the expat holds within his/her home country and in China.

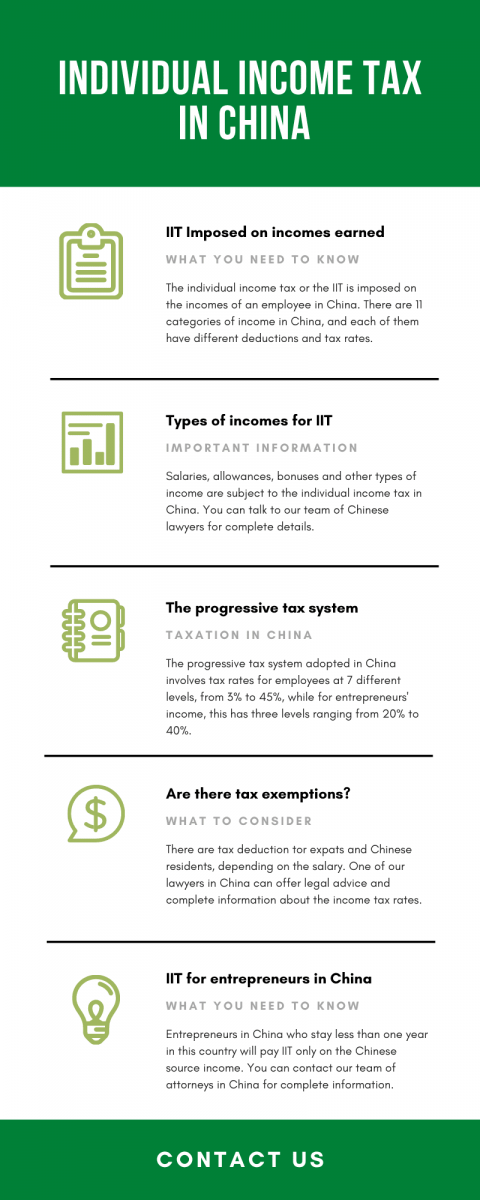

In this country, Individual Income Tax Law presents eleven categories of income, each of it having different deductions, tax rates, and exceptions that apply to each of them. Our Chinese lawyers can offer detailed assistance on the matter if you are interested in the conditions of China income tax and related aspects.

Table of Contents

The level of income in China

The parts of the expat’s remuneration deemed to be taxable income by Chinese local authorities are the base salary, cash allowances, contributions to an overseas insurance scheme and incentive compensations (commissions and bonuses). Moreover, the taxation rate levied on taxable income depends on its total amount accumulated. A progressive tax system is adopted in China where the tax rate for employees progresses in seven levels from 3% to 45% whereas for entrepreneurs’ income it has three levels, from 20% to 40%.

Tax exemptions for expats (4800 RMB – Chinese currency, Renminbi) and for Chinese residents (3500 RMB) are granted from their wages. In addition, for each individual taxation rate, there is a quick deduction amount which will be exempted for this level of taxable income. Individual income tax amount in China is calculated as it follows:

(Gross Monthly Taxable Income– 4800 RMB) * Tax Rate.

Our attorneys in China can provide further details regarding China income tax and other useful information. Here is an infographic with extra details:

Duration of stay in China and payment source

In order to determine if a foreign individual working in China is subject to IIT, it is necessary to look at the amount of time spent in China, the source of income and where the employer is based. Consequently, foreign entrepreneurs residing in China for less than 12 months are subject to IIT on their Chinese-source income only. Salaries, from international employers to individuals working here, are exempt from tax if the individual stays in China for less than 90 days per year on the condition that the remuneration is paid or borne by a Chinese establishment.

The 90-day period can be extended to 183 days if the individual has the right to protection under a relevant tax arrangement or treaty. On the other hand, in order to reduce tax liability, if certain conditions are fulfilled, employees of foreign employers can be taxed based on the number of days of residence in China. Our lawyers in China will provide further tips and information regarding IIT.

Entrepreneurs who only reside here (with no domicile in China) between 1 to 5 years must pay IIT for income received from both foreign and Chinese employers for work conducted here (China-sourced income) and for income paid by domestic employers during temporary absences from China. Furthermore, from the sixth year onward, foreign individuals will be taxed on their global income for each year of residence in China.

The income categories in China

The IIT is imposed on a single income category, and here we mention 9 important types:

- Wages and salaries.

- Rental income.

- Labor services remuneration.

- Business income.

- Profit distribution, dividends, interest.

- Incidental income

- Royalties.

- Incomes derived from property transfer.

- Author’s remuneration.

It is important to note that some of the above-mentioned types of incomes are levied on a yearly basis, according to the Tax Law in China. This rule applies to residents in China, while non-residents are subject to monthly taxation for any type of income. Foreigners in China must pay attention to the tax structure imposed in this country and are suggested to talk to a Chinese lawyer for comprehensive information, so they can be prepared from a tax point of view. If you need extra details about China income tax, feel free to get in touch with our specialists.

Progressive tax rates for IIT calculation

Residents in China must pay taxes on incomes, reminding them that the taxation is made annually. We present you a table with the tax rates on annual taxable incomes in local currency, plus quick deduction:

| Annual Taxable Income | Applicable Tax Rate | Quick Deduction |

| Between 0 and 36,000 | 3% | 0 |

| From 36,000 to 144,000 | 10% | 2,520 |

| From 144,000 to 300,000 | 20% | 16,920 |

| From 300,000 to 420,000 | 25% | 31,920 |

| From 420,000 to 660,000 | 30% | 52,920 |

| From 660,000 to 960,000 | 35% | 85,920 |

| More than 960,000 | 45% | 182,920 |

In the case of non-residents in China, the following tax rates apply:

| Monthly Taxable Income | Applicable Tax Rate | Quick Deduction |

| Between 0 and 3,000 | 3% | 0 |

| From 3,000 to 12,000 | 10% | 210 |

| From 12,000 to 25,000 | 20% | 1,410 |

| From 25,000 to 35,000 | 25% | 2,660 |

| From 35,000 to 55,000 | 30% | 4,410 |

| From 55,000 to 80,000 | 35% | 7,160 |

| More than 80,000 | 45% | 15,160 |

FAQ about IIT in China

1. How is the Individual Income Tax imposed on personal incomes in China?

IIT is imposed on incomes derived in China, depending on the amount of money gained, length of stay, and other important considerations that can be explained by one of our Chinese lawyers.

2. What types of incomes are subject to IIT in China?

Salaries, wages, royalties, dividends, incomes derived from property transfers in China, author’s remuneration, rental incomes are among the types of incomes taxed in China.

3. Are tax exemptions for incomes in China?

Yes, in the case of foreigners with incomes of CNY 4,800 there is no IIT. The same is available for incomes of CNY 3,500 registered by Chinese residents.

4. How is a sole proprietorship taxed in China?

Progressive tax rates ranging from 5% to 35% apply to incomes registered by partnerships, sole proprietorships, and privately-owned businesses. More in this matter can be discussed with our attorneys in China.

5. How is the flat tax rate of 20% applied in China?

A tax rate of 20% applies to capital gains, rental incomes, dividends, or interest incomes. These are other types of personal incomes for which one must pay taxes in China.

Short facts about working in China as a foreigner

Overseas entrepreneurs can easily start their activities as sole proprietorships, one of the most popular and simple business structures available in China. Cities like Shanghai, Guangzhou, Shenzhen, and Beijing are quite representative from a business point of view and often on the list of international entrepreneurs or small business owners. Sectors like tourism, food, IT, energy, engineering, and innovation are prolific in China and quite generous from a business point of view. Being a huge business and financial destination, China is extremely appealing for foreigners wanting to develop their activities here, however, the language barrier might be an obstacle. Nevertheless, it is advisable to get in touch with our law firm in China if you would like to know more about how to start a business in China and about the taxation in this county.

- Here are some interesting facts and figures about the economy and business in China that you might find interesting:

- Nearly USD 1,769 billion represented the total FDI stock in China in 2019.

- China ranked 31st out of 190 worldwide economies, according to the 2020 Doing Business report.

- China was the second-largest FDI recipient in 2019, after USA and followed by Singapore.

Please contact our Chinese team of lawyers if you need assistance and documented guidance on China income tax.